Dreaming of days spent out on the water, the sun on your face, and the wind in your hair? Owning a boat can be a fantastic experience, but the financial aspect can often feel overwhelming, especially for those with lower incomes. Is financing a boat even possible when you're working with a tight budget? That’s the question we’re diving into today. It's a common concern, and one that deserves a thorough exploration.

Securing a boat loan with a limited income can certainly be challenging, but it's not necessarily impossible. Lenders consider various factors beyond just your income, such as your credit score, debt-to-income ratio, and the type of boat you're looking to purchase. Understanding how these factors interplay is key to navigating the loan application process successfully.

The landscape of boat financing has evolved over time, reflecting broader economic trends and lending practices. Historically, obtaining any loan with a lower income was difficult. Today, while challenges persist, there are more options available, and lenders are sometimes more willing to consider individual circumstances. However, the increased availability of loans doesn't diminish the importance of responsible borrowing and careful financial planning.

The core issue revolving around boat loans for lower-income individuals is the perceived risk for lenders. Boats, unlike houses or cars, are often considered luxury items, and their value can depreciate. Lenders want assurance that borrowers can reliably make payments, regardless of income level. This is why credit history and debt management become even more critical in these situations.

So, what can you do to improve your chances of getting approved for a boat loan with a low income? First, focus on strengthening your credit score. Paying bills on time, keeping credit utilization low, and addressing any errors on your credit report can significantly impact your creditworthiness. Building a solid credit history demonstrates responsible financial behavior, which can reassure lenders.

Saving for a substantial down payment is another crucial step. A larger down payment reduces the loan amount and signals to lenders that you're committed to the purchase. It also lowers your monthly payments, making them more manageable within your budget.

Exploring different loan options is essential. Consider credit unions or smaller banks, which may have more flexible lending criteria than larger national institutions. Also, research various loan types, such as secured loans, which use the boat as collateral, or personal loans, which may have higher interest rates but offer more flexibility.

Consider buying a used or less expensive boat. A smaller, more affordable boat can significantly reduce the loan amount needed, making it easier to secure financing and manage monthly payments.

Advantages and Disadvantages of Boat Loans with Low Income

| Advantages | Disadvantages |

|---|---|

| Potential to fulfill boating dreams | Higher interest rates |

| Building credit with responsible repayment | Risk of repossession |

| Enjoyment and recreational benefits of boat ownership | Difficulty getting approved |

Frequently Asked Questions:

1. What credit score is needed for a boat loan? It varies by lender, but generally, a score above 650 is desirable.

2. Can I get a boat loan with bad credit? It's more challenging, but some lenders specialize in subprime loans.

3. What is the typical interest rate for a boat loan? Rates depend on factors like credit score and loan term.

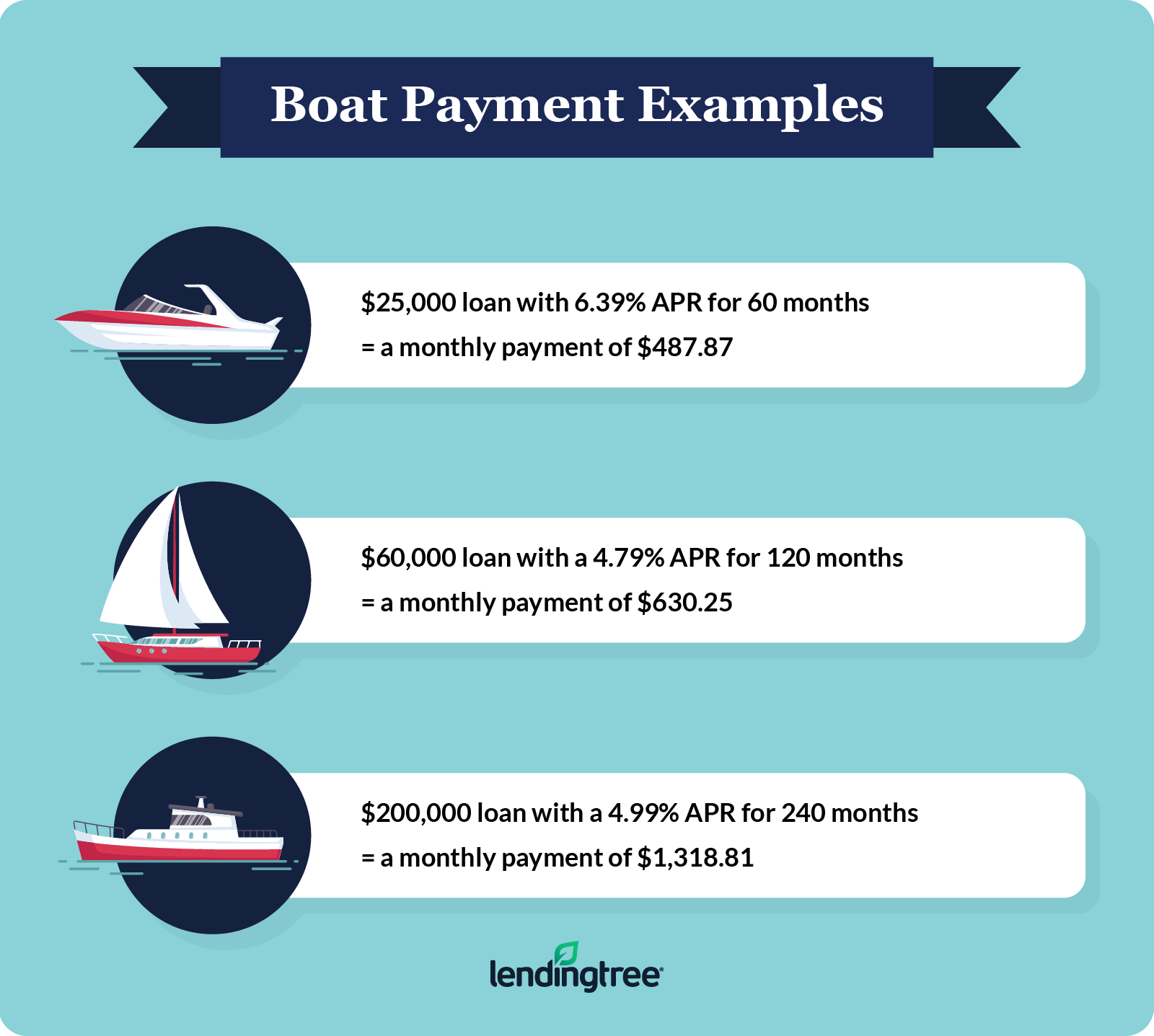

4. How long are boat loan terms? They can range from a few years to 20 years or more for larger loans.

5. What is the down payment required for a boat loan? Lenders may require 10-20% or more, especially with lower incomes.

6. Can I refinance my boat loan later? Yes, refinancing can be an option to secure a lower interest rate.

7. Are there boat loan calculators available online? Yes, many online calculators can help estimate monthly payments.

8. Should I get pre-approved for a boat loan? Pre-approval can help you understand your budget and strengthen your offer when buying.

Securing a boat loan with a low income requires careful planning, research, and a realistic assessment of your financial situation. While it presents challenges, it's not an insurmountable hurdle. By understanding the factors lenders consider, strengthening your credit, saving for a down payment, and exploring various loan options, you can increase your chances of realizing your dream of boat ownership. Remember, responsible financial planning is key to enjoying your boat without the burden of overwhelming debt. Don’t let your income define your aspirations; with careful navigation and informed decision-making, you can chart a course toward owning the boat you’ve always wanted.

Unlock the fun exploring the world of free online survey games

Chai hu shu gan wan unraveling the mystery of the american dragon

Maximize your twitter presence the ultimate guide to twitter pfp pixel dimensions

7 Easy Ways To Get Low Income Grants - You're The Only One I've Told

Different Types Of Investment Property Loans The Ultimate Guide - You're The Only One I've Told

Letters Roundabout at downtown Manaus Brazil Manaus Amazonas - You're The Only One I've Told

Housing corp affordable housing for special needs families in houston - You're The Only One I've Told

Minimum Income To Qualify For Obamacare 2024 - You're The Only One I've Told

Who Qualifies For Low Income Housing In Florida All Answers - You're The Only One I've Told

Boat Loans Frequently Asked Questions - You're The Only One I've Told

Can You Get Low Income Housing With No Income at Katherine Perkins blog - You're The Only One I've Told

are boat loans hard to get with low income - You're The Only One I've Told

What is classed as a low - You're The Only One I've Told

Figure 23 from Optimizing the Performance of a Manually Operated - You're The Only One I've Told

Boat Financing How To Finance A Boat - You're The Only One I've Told

Common Jack Russell Terrier Health Issues - You're The Only One I've Told

Everything You Need to Know About Low - You're The Only One I've Told

Mark Klimek NCLEX Review - You're The Only One I've Told